Greece has been an “economic problem” for some time.

And being in a single currency union has made the situation worse.

Other Eurozone countries, hoping to avoid further defaults, have provided Greece with extensions on debt amortization and interest payments.

But it remains unclear how Greece can survive without continued support.

Introduction

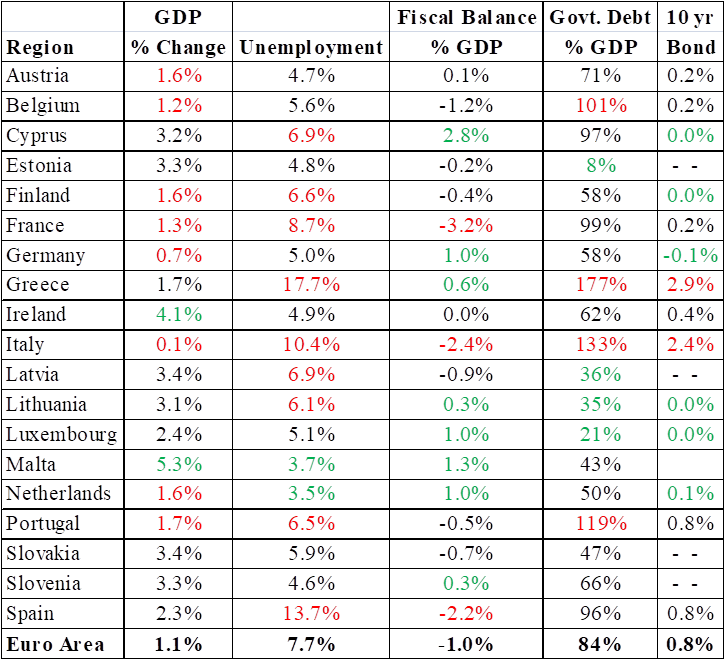

The economic prospects for the Eurozone are not good: slow growth, lagging investments and high unemployment levels. Projected GDP growth this year is projected at only 1.2% with unemployment for the region averaging 7.7%. There are continual worries/uncertainties about Brexit, but the poster child for Eurozone malaise is Greece. Below, the Greek problem is described and related to the overall Eurozone region.

The Eurozone

According to FocusEconomics, Eurozone GDP growth is weak, projected at only 1.1% for the year. The German and France economies, by far the largest in the region, are only projected to grow by 0.7% and 1.3% respectively. And Italy, the 3rd largest, will only grow 0.1% this year. For many countries, unemployment is a serious problem, particularly in Greece (17.7%), Spain (17.7%) and Italy (10.4%).

Countries already projected to large government deficits will have little “fiscal policy room” to deal with their unemployment. France and Italy are running the largest government deficits. Large government debts are also worrisome. And here, Greece with debt at 177% of GDP is in a class by itself. But debts in Italy and Portugal need to be watched.

The 10-year government bond rates are included in Table 1 to indicate the importance of the European Central Bank’s (ECB) intervention. Given the perilous condition of some of these countries, they could never borrow at these rates without substantial outside support.

Table 1. – Eurozone Country Indicators, 2019

Source: FocusEconomics

A problem with the Eurozone that few people understand stems from the fact that all countries use the same currency. And why is this a problem? Because it takes away a critical adjustment mechanism that keeps international trade in balance. Consider this example from the US-Japanese experience:

In 1970, there were ¥350 to the dollar. Now, there are only ¥109 to the dollar. The dollar depreciation made up for the higher productivity of Japan by making US products cheaper to Japan and Japanese imports more expensive to Americans.

Like the US several decades back, Greece is not as “productive” in making goods as, say, Germany. If Greece had its own currency, it would weaken until its goods were competitive with the German’s products. That would keep trade among countries in balance. But in this single currency zone, that adjustment is not available. The consequence is that countries can run up huge trade deficits and literally run out of Euros. That is what happened to Greece. And it borrowed to make up the difference until no investor would lend it more Euros.

So move ahead to today. The economically strong countries in the Eurozone, led by Germany, are trying to reduce aggregate demand in Greece by forcing the country to run large fiscal surpluses. The hope is that the resulting demand reduction will reduce import demand and bring its international trade back into balance. This is unlikely to succeed. It was tried before, resulting in the Greek unemployment rate spiking to 27.5% in 2013.

So for the countries in the Eurozone, large trade deficits, without capital inflow offsets, can be a precursor to a country literally running out of “money.” Table 2 provides data on Eurozone countries’ international trade balances. For countries to avoid running out of Euros, capital inflows must exceed their trade deficits. Eurozone country assistance is all that is keeping Greece “afloat.”

Table 2. – International Trade Balances, Eurozone Countries, 2018

Source: FocusEconomics

The Greek Situation

First, a little history:

When the Greek unemployment rate hit 27.5%, the IMF gave up on austerity and pressed for a large number of Greek reforms. Further, it told the European countries that further debt forgiveness would be required. Nothing has really changed since then. The key players remain the same: The Greek government, Germany as the leader of the ECB/EC bloc and the IMF. The Greek government is forced to agree with what is needed to get financial support. It then delays implementation. The EU continues to insist on austerity and no forgiveness. The IMF keeps pressing for reforms and a second round of debt forgiveness.

Today, the strong Eurozone countries, led by Germany, are forcing Greece to run large fiscal surpluses. At the same time, they are bending over backwards to provide the country with financial support. This support is not a reflection of concern for the Greek people. Rather, it is provided to help banks that foolishly invested in Greek government debt. Banks do not like debt defaults and the hope is that Greece can somehow avoid more defaults. Will this strategy work?

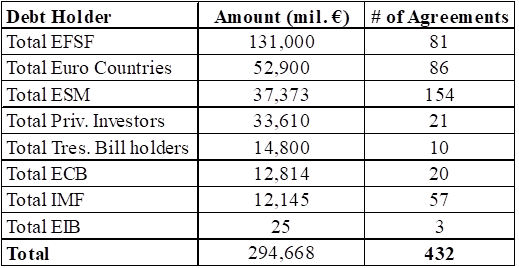

Table 3 gives a partial listing of Greek debt.

Table 3. – A Partial Listing of Greek Debt

Source: Wall Street Journal

The latest bailout program for Greece includes:

- A 10-year extension on the maturity dates of €96.4 billion in loans.

- A 10-year extension on subsidized interest payments on its debt.

- € 15 billion to boost its cash reserves.

In addition, the European Financial Stability Facility (EFSF) has reimbursed the €103 million step-up margin paid by Greece for the period between January and June 2018 and cancelled the 2% step-up margin payable on certain EFSF loans. Greece’s total benefit from these actions will be €329 million. Further, the European Stability Mechanism (ESM) will transfer another €644 million to Greece.

In return, Greece agrees to run primary budget surpluses of 3.5% until 2022, and then by about 2.2% until 2060.

To give you some idea of how important the EU support is for Greece, consider data presented in Table 4. Greece’s public debt is now €334.4 billion. Greece is paying only €7.1 billion in interest meaning the effective rate on its debt is only 1%. Greece is running a government surplus of 1.4%.

Suppose the interest rate were 6%, a reasonable number considering uncertainties in Greece. Interest payments would then be €20 billion resulting in a fiscal deficit of €11.8 billion or 6.2% of GDP.

My conclusion: It is not at all clear how the subsidies to Greece can be removed without a major debt forgiveness.

Table 4. – The Greek Situation: With and Without Support

Source: FocusEconomics

I quote from a recent IMF staff report:

“… the debt relief recently agreed with Greece’s European partners has significantly improved debt sustainability over the medium term, but longer-term prospects remain uncertain. The extension of maturities by 10 years and other debt relief measures, combined with a large cash buffer, will secure a steady reduction in debt and gross financing needs as a percent of GDP over the medium term and this should significantly improve the prospects for Greece to sustain access to market financing over the medium term. Staff is concerned, however, that this improvement in debt indicators can only be sustained over the long run under what appear to be very ambitious assumptions about GDP growth and Greece’s ability to run large primary fiscal surpluses, suggesting that it could be difficult to sustain market access over the longer run without further debt relief. In this regard, Staff welcomes the undertaking of European partners to provide additional relief if needed, but believe that it is critically important that any such additional relief be contingent on realistic assumptions, in particular about Greece’s ability to sustain exceptionally high primary surpluses.”

Conclusions

The Eurozone is beset with problems: slow growth, high unemployment and the stark and serious uncertainty on how Brexit will be resolved. And as outlined above, having a large number of countries using the same currency has inherent weaknesses. The Greek case demonstrates these weaknesses. And it is not at all clear how Greece will survive without massive outside support.

{kind=link}